Mergers and acquisitions (M&A), spinouts, divestments and the like – are a vibrant element of business that have hit public consciousness thanks to the likes of shows such as Succession and Billions.

In the real world, business has been brisk. We have seen $559bn global M&A market values in Q1 2023 and 1,166 active spinouts reported in the UK in 2022. These numbers show that the market remains incredibly active even amidst a slowdown.

But on-screen or off, these transactions are no place for the faint of heart. Transactions demand world-class attention to detail and confident direction – especially when it comes to the technology that underpins the valuation of a company.

Digital due diligence – the starting point of visibility

Regardless of being sell or buy side, visibility and confidence in the technology involved in any transaction arise only from keen digital due diligence (DDD).

‘Traditional’ due diligence is classified as the investigation, audit, or review performed to confirm facts or details of a matter under consideration. In the financial world, due diligence requires an examination of financial records before entering into a proposed transaction with another party.

Digital due diligence is the application of this rigour to business operations, ways of working, and, specifically, the technology used.

Why does digital due diligence exist?

The evolution to digital due diligence is the inevitable result of businesses becoming digital-by-default. It is the recognition that just as technology underpins all business functions, it is the basis of an accurate company valuation.

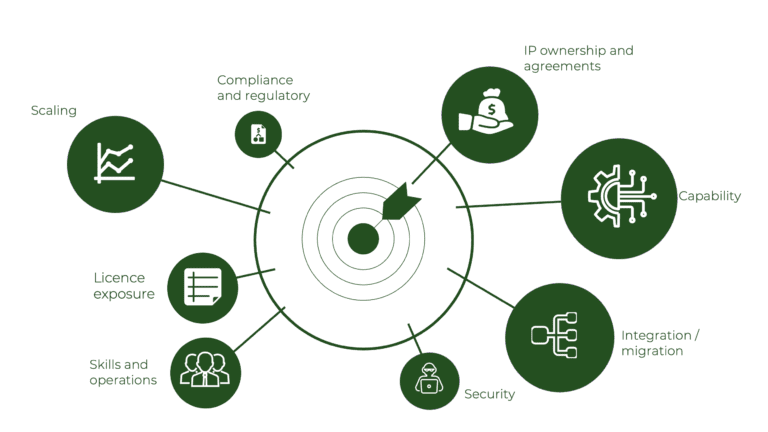

One of the most pressing initial questions is how the target company assesses their technologically held IP. Early, awkward attempts at assessing have typically focused on a company’s “digital assets”. This was often limited to websites or even search rankings.

This is, however, woefully inadequate for most businesses. To be of any real use, digital due diligence must encompass the impact of digital on how a business operates. For example, in the case of data that is vital to operations, is it owned by the target or a third party? How can the new owners ensure they retain access to that data, and at what cost? Systems engineering is another consideration: in acquiring a company, it is imperative to have a clear grasp of the processes in place.

Moving to value creation

This will quickly lead to one of the golden questions: How much provision needs to be made to maintain critical business operations? i.e., what does it take to keep things going as they are?

One step further in this discussion opens up the possibility of value creation. It is often assumed that increased value will automatically follow from the constructive collaboration of two companies. However, this is myopic. It is important to have visibility of the costs of any value creation. Indeed, a close analysis of the necessary investment to release value in an acquisition could make a case to alter the valuation.

For example, in one recent project, we found that there was a substantial difference between the payment and point-of-sale systems between the target and the acquiring company. To effect a smooth transition, there needed to be a substantial investment of time and money in training users on new systems.

The other consideration in early-stage value creation is to identify the pet projects of the previous business owners. All too often, experience shows that substantial value can be realised by interrogating and then modifying (or eliminating) vanity projects sustained solely because management has liked them.

It is all too often the case that such projects are not set to return anywhere near the value they have been promoted as promising – so a keen part of the change management of the transition is to see these projects either retired or refined into something more likely to create value.

Be it on the small screen or the boardroom, transactions often represent the more dramatic end of business – but drama is often the enemy of the consistency, diligence, and management of multiple third parties that makes a successful M&A, spinout, or divestment. If you are exploring merger, acquisition, divestment or spinout options, check out more of our insight and experience at BML.Ventures.